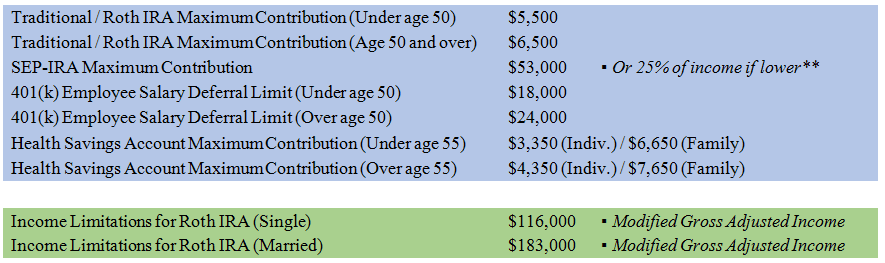

Welcome to tax season 2016. At this point, you should have received your tax statements and have probably either met with or are scheduled to meet with your tax preparer. Have you made your 2015 contribution to your IRA yet? Do you need to establish a new Traditional IRA, Roth IRA or SEP-IRA? Do you want to make a 2015 tax-deductible contribution to a Health Savings Account (HSA)?

In an effort to inform you of the specific deadlines for your 2015 contributions and to help you better understand which types of plans may be most appropriate and beneficial for you, we have created the following break-down of the deadlines, contribution limits and other details that can impact your contributions for the 2015 tax year.

Also, please be advised that the deadline for on time tax filing and for all 2015 IRA plan contributions is Monday, April 18th this year*.

Participation in your company’s sponsored retirement plan (401(k), 403(b), etc.) does not affect your ability to make a Traditional or Roth IRA contribution. However, if your modified adjusted gross income exceeds $61,000 (single) or $98,000 (married), then your ability to deduct your Traditional IRA contribution begins to phase out. If you don’t contribute to a corporate plan but your spouse does, the deduction phase-out begins at $183,000.

Contribution eligibility for a Traditional IRA stops at age 70.5, but you may still contribute to a Roth.

Are you potentially considering converting a pre-existing Traditional IRA into a Roth IRA? If you exceed the income ceiling for contributing to a Roth IRA, you are still eligible to convert your Traditional IRA account at any time regardless of your income. The taxes owed on the original contributions and any investment gains will be calculated prior to conversion and the taxes will be due in the calendar year of the conversion. Because the taxes due are assessed at your income tax rate for the year of conversion, it may make sense to consider converting in a lower income year. The long-term benefits of conversion can be significant if there are several years (or decades) to go until those contributions are taken as withdrawal benefits. Do you want to contribute to a Roth IRA but your income exceeds the limit? We can make a non-deductible Traditional IRA contribution, and then convert to a Roth IRA.

* SEP Extensions

** Some exceptions may apply, please cross reference your specific situation with your tax preparer.