From Market Fragility to Portfolio Durability

As we wrap up the year, we reflect on our 2024 outlook, “Prepare, Not Predict,” and the dynamic and unpredictable nature of the financial markets. Our 2024 themes manifested with varying impact. Inflation remained in the Messy Middle and stabilized within a manageable range. The Federal Reserve (the Fed) ultimately began to cut interest rates in September, which brought fixed income yields broadly lower from 2023. In 2023, we emphasized the importance of Preparation over Prediction, a sentiment that proved prescient as we navigated a landscape marked by continued volatility, unexpected geopolitical events and a presidential election. Yet markets broadly performed quite well, and the economy remains resilient, despite the recent uptick in unemployment. Our third theme of Concentrated Consequences carries through as we turn towards 2025. We highlighted the fragility within U.S. equities, driven by the narrow leadership of the “Magnificent 7” and the potential for opportunity in areas beyond U.S. large-cap equities. That narrative only intensified and by November 30, 2024, the top 10 stocks of the S&P 500 accounted for 35% of the index, up from 31% at the start of the year[1]. Still, green shoots remain. Small caps outpaced large caps for the one-year period ending November 30, 2024[2]. As we step into 2025, our focus sharpens on resilience and adaptability that empower us to navigate any fragility that may lie ahead.

2025 Themes

Markets stand at a fascinating crossroads. While opportunities and optimism remain, the path forward for allocations is anything but straightforward. This year, our outlook centers on three pivotal themes: fragility, durability and the age of alpha. Fragility captures the vulnerabilities embedded in global markets derived from full valuations, concentration and inflationary pressures. It is a call for caution and strategic foresight to mitigate risks. Durability shifts the focus to building resilience through thoughtfully diversified asset allocations designed to withstand today’s risks and position portfolios for long-term success. Finally, The Age of Alpha highlights the growing potential of active management and alternative investments to drive outcomes in a market where traditional beta opportunities are scarce. Together, we believe these themes provide a framework for addressing uncertainty while identifying opportunities to enhance portfolio resilience and performance.

Fragility

Elevated valuations, intensified market concentration and the risk of a second wave of inflation sow the seeds of vulnerability in markets today. Both equity and fixed income valuations hover at precariously high levels. U.S. equity markets have surged in 2024, with the S&P 500 Index gaining 28.1% through November[3]. Valuations for the index, as measured by price-to-earnings ratio, sit above 22x, close to the 20-year high and more than one standard deviation above the long-term average[4]. When compared globally, U.S. large-cap equities appear even more stretched relative to their non-U.S. counterparts, adding a layer of risk for investors overly concentrated in this space. Meanwhile, in the bond market, credit spreads (one valuation measure for fixed income) have compressed close to levels last seen before the ’07-’09 financial crisis.

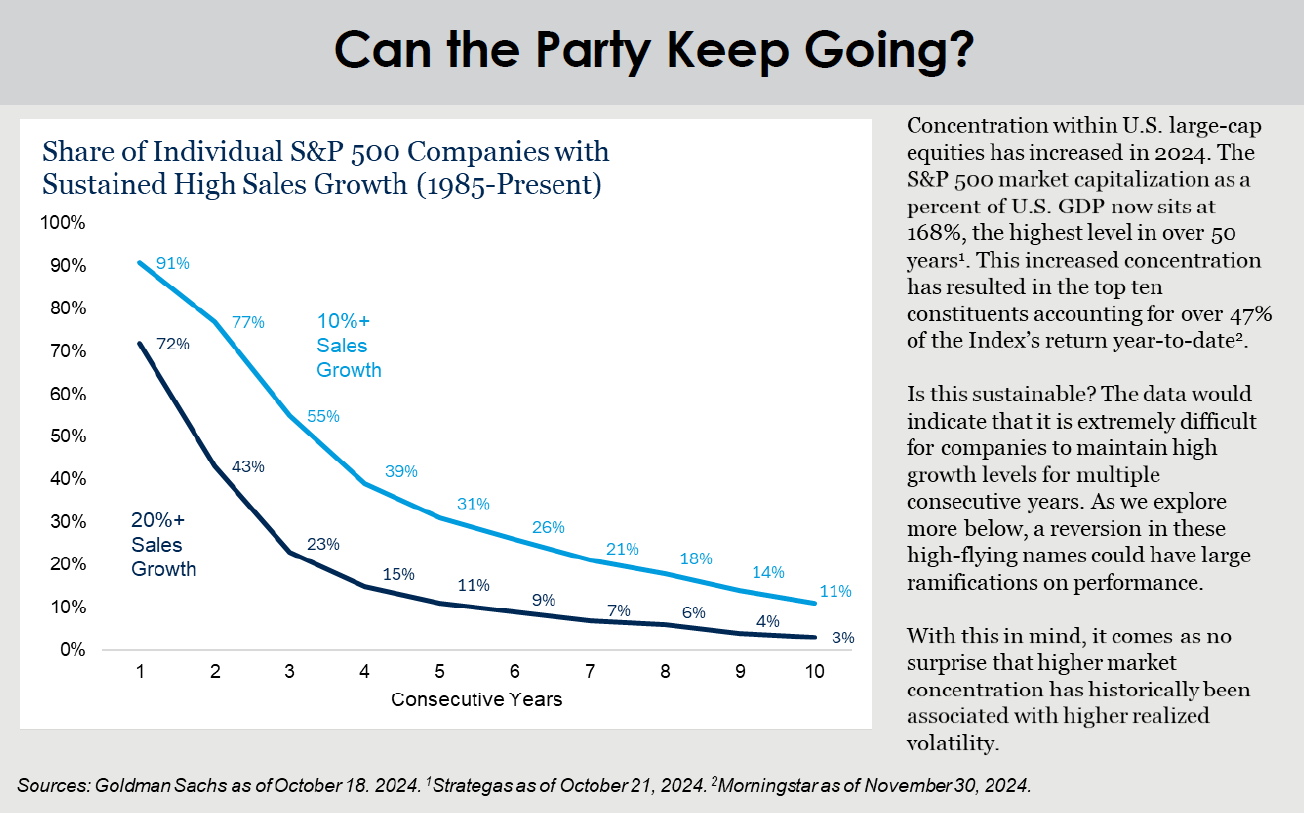

Fueling a portion of these valuations has been the continued strength of large cap companies concentrated at the top of the market. This narrow market leadership means that the fortunes of a handful of companies disproportionately influence the broader market. Any misstep—be it a disappointing earnings report or adverse development—could lead to significant volatility.

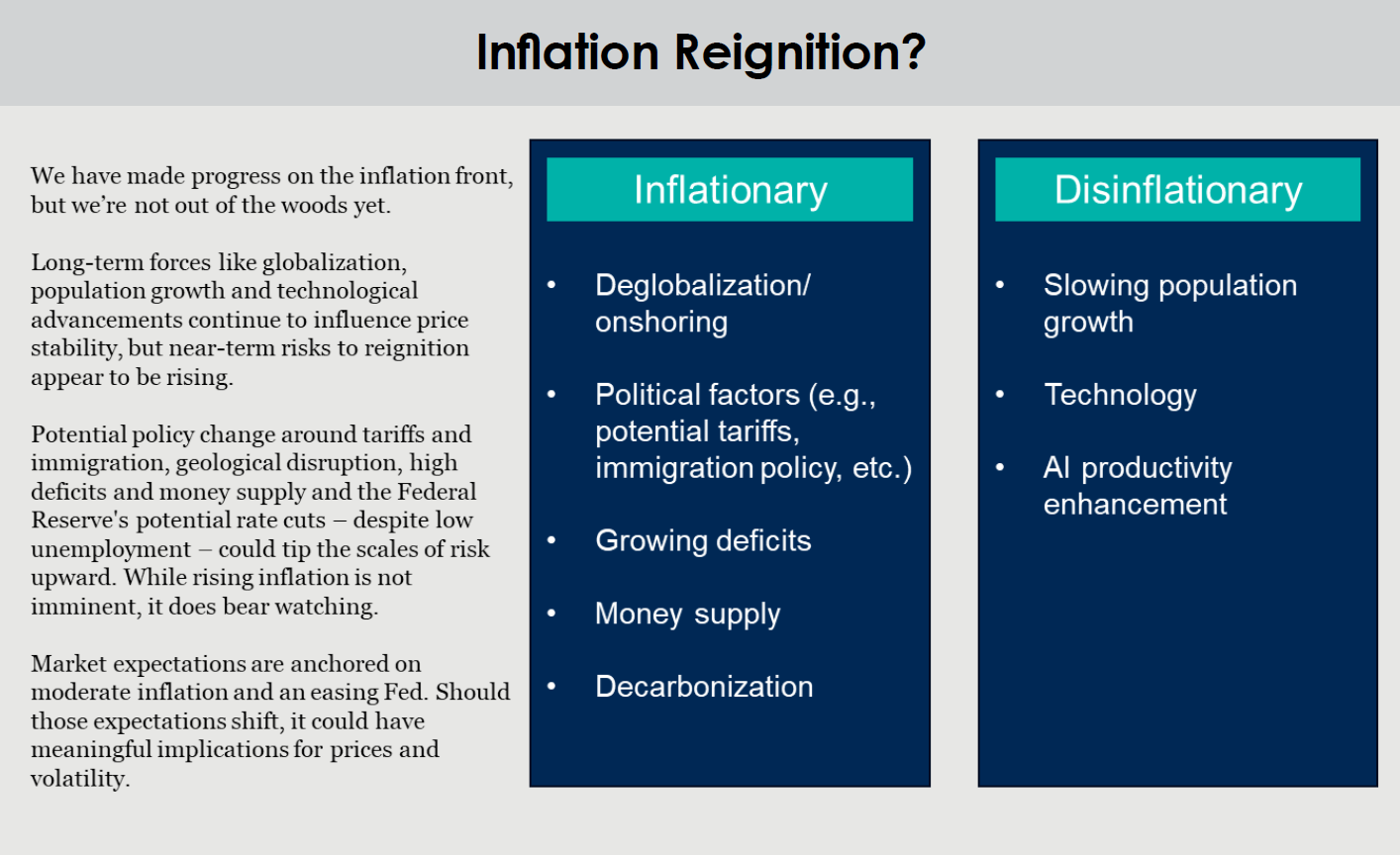

Further adding to the complexity is the threat of reinflation. While inflation has eased in recent years (U.S. CPI now sits at 2.6%[5]), it has not vanished, and there are potential rising inflationary pressures. Should reinflation materialize, it could upend expectations for financial markets.

Portfolio Impact:

High valuations in both equity and fixed income markets, coupled with market concentration and the growing risk of reinflation, have created a fragile market environment. As we look ahead, navigating this landscape requires a disciplined approach. With limited clear-cut opportunities – what some may call “fat pitches”- in today’s market, it may not be the time to take undue risk in portfolios. Rather, consider strategies that balance opportunity with durability. Diversification, reevaluation of risk tolerances, careful selection of asset managers and a keen eye on market developments will be essential in navigating 2025.

Durability

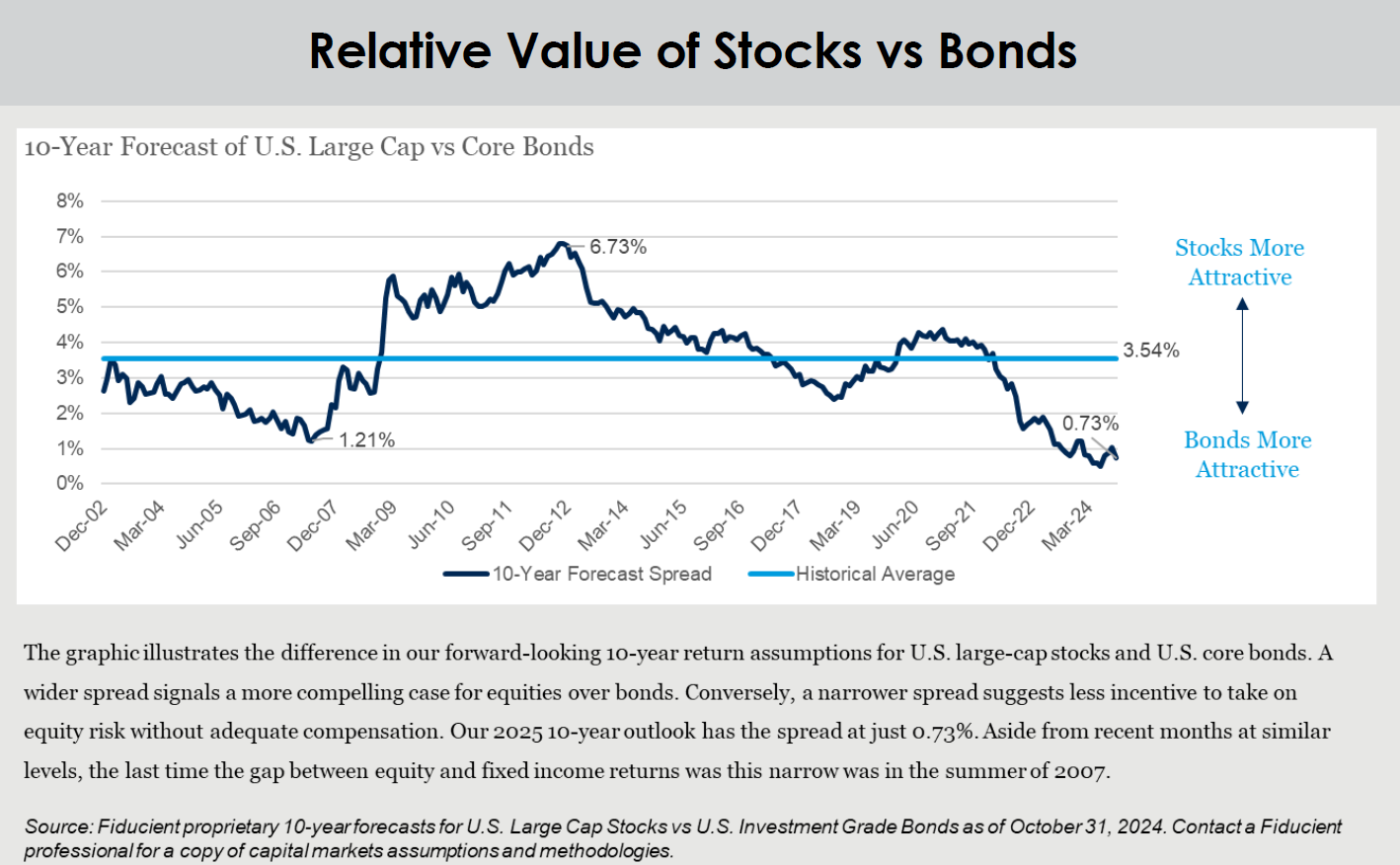

Investing is synonymous with taking risk and there are few, if any, investments that generate sufficient returns without it. While the risks we outlined above are not new to investing, they are particularly pronounced in today’s market. We believe this makes portfolio durability more critical than ever. The good news? Building a durable portfolio comes at a surprisingly modest “cost” for long-term investors. As we demonstrate below, the gap between our forward return expectations for fixed income and U.S. equities is the smallest it has been since 2007. Furthermore, incorporating global equity allocations may enhance durability by mitigating the acute concentration risks often seen in U.S.-centric portfolios.

Portfolio Impact:

Before simply shifting allocations from stocks to bonds, it is important to consider several factors. First and foremost, a portfolio’s allocation should align with its long-term objectives. While minor adjustments may be appropriate, wholesale changes should only follow a fundamental shift in those goals. Moreover, reviewing your goals and risk tolerance is most effective when done proactively during calm market periods rather than times of volatility. With markets experiencing substantial gains in recent years, it is an opportune time to reaffirm or refine your portfolio’s objectives. We encourage investors to evaluate current portfolio allocations in light of recent returns with a focus on the relative positioning of stocks and bonds.

The Age of Alpha

We believe three factors have converged making active management and alternatives more compelling today:

- Valuations: With U.S. markets trading at elevated valuations, our forward 10-year return forecast is a modest 5.6%[6]. We believe this presents a relatively low hurdle for alternative investments to outperform while potentially reducing exposure to full market risk.

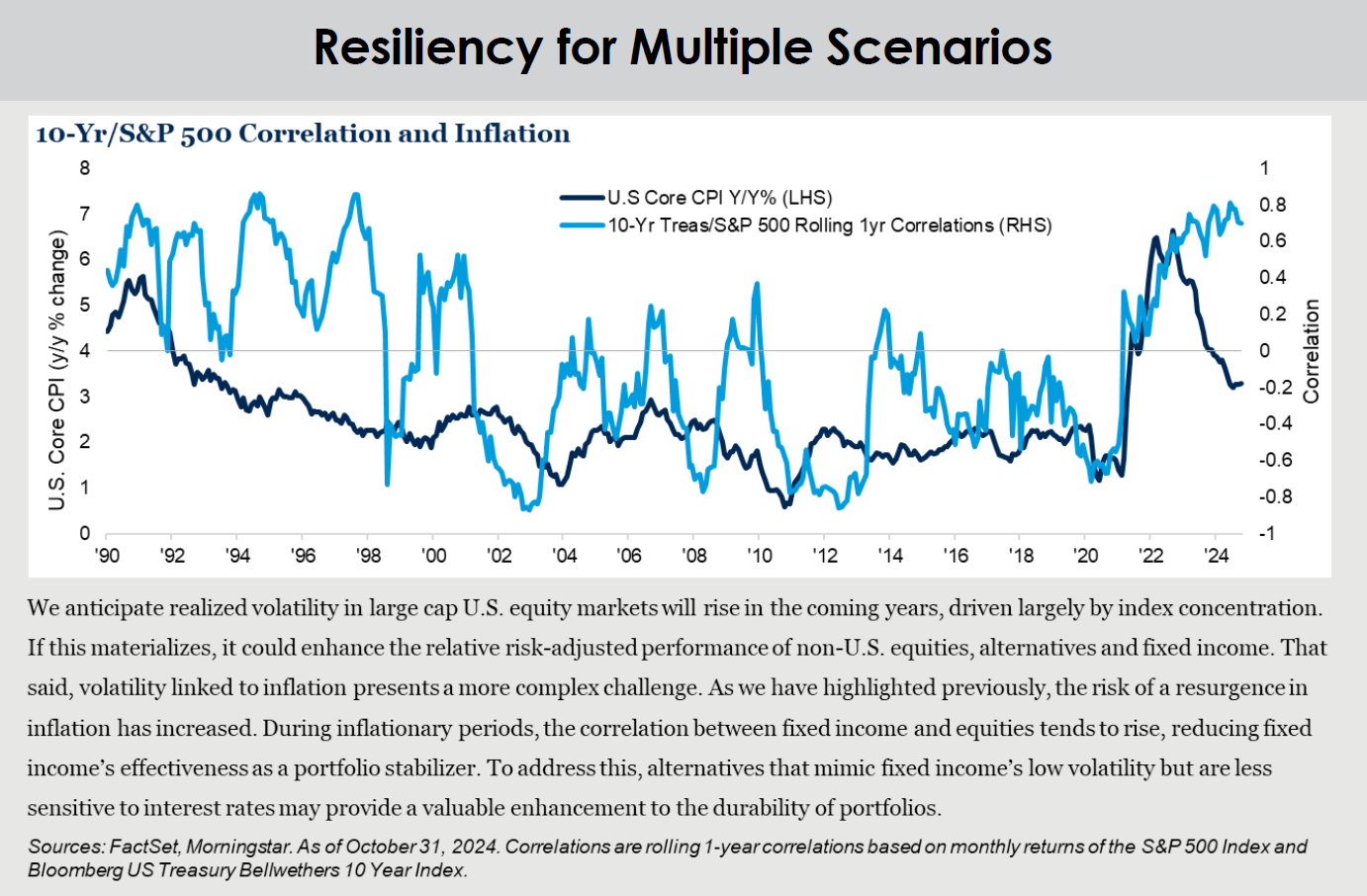

- Concentration: A heavy reliance on a handful of stocks increases the overall risk for broader markets to sustain recent performance.

- Volatility: Higher market concentration typically results in increased volatility and inflation volatility may reduce the diversification of some traditional assets. Volatility has important impacts on asset allocation, but it also creates fertile ground for stock selection and targeted opportunities for active management.

Portfolio Impact:

The combination of full valuations, concentrated markets and the possibility of a renewed inflationary cycle sets the stage for alternative asset classes, active management and thoughtful portfolio construction to enhance durability.

As part of our 2025 strategy, we are increasing allocations to dynamic fixed income and Treasury Inflation-Protected Securities (TIPS) while eliminating exposure to global fixed income. Given the relative appeal of other fixed income opportunities and the potential for heightened currency volatility, we believe global fixed income has a less compelling value proposition.

We also suggest clients evaluate the inclusion of alternative investments, such as hedge funds and private markets, in their portfolios. While these strategies may not suit all investors—particularly those with constraints related to liquidity or allocation size—they represent a compelling opportunity in today’s environment.

Within real assets, we are maintaining our overall weighting but shifting toward a more diversified allocation. The potential for inflationary pressures—driven by unpredictable factors like military conflict and policy changes, for example —underscores the importance of holding a broad array of real assets to hedge against unexpected inflationary spikes.

Final Thoughts

Full valuations, index concentration and the potential for a resurgence of inflation have set the stage for a fragile market environment. Can prices rise further from here? Absolutely. Yet the possibility of setbacks is equally real, underscoring the importance of durability as we head into 2025.

This year, intentionality is key. Reaffirming portfolio positioning and risk exposure is a prudent annual exercise, particularly in light of recent market gains. While timing markets is inherently fraught, the relatively modest long-term trade-off between equity and fixed income forecasts opens the door to thoughtful conversations about portfolio posture.

Mitigating acute risks, such as concentration and inflation, calls for thoughtful diversification—leveraging global equity allocations, tailored fixed income strategies and a broader spectrum of investments. Moving beyond passive and traditional approaches into active management and alternatives has the potential to enhance portfolio resilience.

We recognize that some of these adjustments may not align with the comfort of chasing what has performed best recently. But as only Cliff Asness can turn a phrase: “Simply looking at historical results and urging investors to ‘buy the thing that’s gone up the most over the long term’ is not financial analysis; it’s finger painting.”

As we look to the year ahead and beyond, our commitment remains steadfast: to make disciplined, forward-looking decisions that empower portfolios to weather uncertainty with the goal of achieving long-term success. For more information, please contact any of the professionals at HCR Wealth Advisors.

[1]. Morningstar, Standard and Poor’s. As of November 30, 2024

[2]. Morningstar. As of November 30, 2024. Small cap = Russell 2000 Index, Large Cap = S&P 500 Index

[3]. Morningstar. Year to date 2024 performance through November 30, 2024.

[4]. FactSet. As of November 30, 2024. Based on forward 12-month price-to-earnings.

[5]. FactSet, Bureau of Labor Statistics. As of October 31, 2024.

[6]. Fiducient proprietary 10-year forecasts for U.S. All Cap Stocks as of October 31, 2024. Contact a HCR Wealth professional for a copy of capital markets assumptions and methodologies

Disclosures and Index Proxies

This report does not represent a specific investment recommendation. Comparisons to any indices referenced herein are for illustrative purposes only and are not meant to imply that actual returns or volatility will be similar to the indices. Indices cannot be invested in directly. Unmanaged index returns assume reinvestment of any and all distributions and are reported gross of any fees and expenses. Any forecasts represent future expectations and actual returns; volatilities and correlations will differ from forecasts.

When referencing asset class returns or statistics, the following indices are used to represent those asset classes, unless otherwise notes. Each index is unmanaged, and investors can not actually invest directly into an index:

INDEX DEFINITIONS

FTSE Treasury Bill 3 Month measures return equivalents of yield averages and are not marked to market. It is an average of the last three three-month Treasury bill month-end rates.

Bloomberg Capital US Treasury Inflation Protected Securities Index consists of Inflation-Protection securities issued by the U.S. Treasury.

Bloomberg Muni 5 Year Index is the 5 year (4-6) component of the Municipal Bond index.

Bloomberg High Yield Municipal Bond Index covers the universe of fixed rate, non-investment grade debt.

Bloomberg U.S. Aggregate Index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

FTSE World Government Bond Index (WGBI) (Unhedged) provides a broad benchmark for the global sovereign fixed income market by measuring the performance of fixed-rate, local currency, investment-grade sovereign debt from over 20 countries.

FTSE World Government Bond Index (WGBI) (Hedged) is designed to represent the FTSE WGBI without the impact of local currency exchange rate fluctuations.

Bloomberg US Corporate High Yield TR USD covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issues from countries designated as emerging markets (sovereign rating of Baa1/BBB+/BBB+ and below using the middle of Moody’s, S&P, and Fitch) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included.

JP Morgan Government Bond Index-Emerging Market Index (GBI-EMI) is a comprehensive, global local emerging markets index, and consists of regularly traded, liquid fixed-rate, domestic currency government bonds to which international investors can gain exposure.

JPMorgan EMBI Global Diversified is an unmanaged, market-capitalization weighted, total-return index tracking the traded market for U.S.-dollar-denominated Brady bonds, Eurobonds, traded loans, and local market debt instruments issued by sovereign and quasi-sovereign entities.

MSCI ACWI is designed to represent performance of the full opportunity set of large- and mid-cap stocks across multiple developed and emerging markets, including cross-market tax incentives.

The S&P 500 is a capitalization-weighted index designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Russell 3000 is a market-cap-weighted index which consists of roughly 3,000 of the largest companies in the U.S. as determined by market capitalization. It represents nearly 98% of the investable U.S. equity market.

Russell Mid Cap measures the performance of the 800 smallest companies in the Russell 1000 Index.

Russell 2000 consists of the 2,000 smallest U.S. companies in the Russell 3000 index.

MSCI EAFE is an equity index which captures large and mid-cap representation across Developed Markets countries around the world, excluding the US and Canada. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

MSCI Emerging Markets captures large and mid-cap representation across Emerging Markets countries. The index covers approximately 85% of the free-float adjusted market capitalization in each country

The Wilshire US Real Estate Securities Index (Wilshire US RESI) is comprised of publicly-traded real estate equity securities and designed to offer a market-based index that is more reflective of real estate held by pension funds.

Alerian MLP Index is a float adjusted, capitalization-weighted index, whose constituents represent approximately 85% of total float-adjusted market capitalization, is disseminated real-time on a price-return basis (AMZ) and on a total-return basis.

Bloomberg Commodity Index (BCI) is calculated on an excess return basis and reflects commodity futures price movements. The index rebalances annually weighted 2/3 by trading volume and 1/3 by world production and weight-caps are applied at the commodity, sector and group level for diversification.

Treasury Inflation-Protected Securities (TIPS) are Treasury bonds that are indexed to inflation to protect investors from the negative effects of rising prices. The principal value of TIPS rises as inflation rises.

HFRI Fund of Funds Composite is an equal-weighted index consisting of over 800 constituent hedge funds, including both domestic and offshore funds.

Cambridge Associates U.S. Private Equity Index (67% Buyout vs. 33% Venture) is based on data compiled from more than 1,200 institutional-quality buyout, growth equity, private equity energy, and mezzanine funds formed between 1986 and 2015.

HFN Hedge Fund Aggregate Average is an equal weighted average of all hedge funds and CTA/managed futures products reporting to the HFN Database. Constituents are aggregated from each of the HFN Strategy Specific Indices.

Goldman Sachs Commodity Index (GSCI) is a broadly diversified, unleveraged, long-only composite index of commodities that measures the performance of the commodity market.

Material Risks Disclosures

Fixed Income securities are subject to interest rate risks, the risk of default and liquidity risk. U.S. investors exposed to non-U.S. fixed income may also be subject to currency risk and fluctuations.

Cash may be subject to the loss of principal and over longer period of time may lose purchasing power due to inflation.

Domestic Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry factors, or other macro events. These may happen quickly and unpredictably.

International Equity can be volatile. The rise or fall in prices take place for a number of reasons including, but not limited to changes to underlying company conditions, sector or industry impacts, or other macro events. These may happen quickly and unpredictably. International equity allocations may also be impact by currency and/or country specific risks which may result in lower liquidity in some markets.

Real Assets can be volatile and may include asset segments that may have greater volatility than investment in traditional equity securities. Such volatility could be influenced by a myriad of factors including, but not limited to overall market volatility, changes in interest rates, political and regulatory developments, or other exogenous events like weather or natural disaster.

Private Equity involves higher risk and is suitable only for sophisticated investors. Along with traditional equity market risks, private equity investments are also subject to higher fees, lower liquidity and the potential for leverage that may amplify volatility and/or the potential loss of capital.

Private Credit involves higher risk and is suitable only for sophisticated investors. These assets are subject to interest rate risks, the risk of default and limited liquidity. U.S. investors exposed to non-U.S. private credit may also be subject to currency risk and fluctuations.

Private Real Estate involves higher risk and is suitable only for sophisticated investors. Real estate assets can be volatile and may include unique risks to the asset class like leverage and/or industry, sector or geographical concentration. Declines in real estate value may take place for a number of reasons including, but are not limited to economic conditions, change in condition of the underlying property or defaults by the borrow.

Marketable Alternatives involves higher risk and is suitable only for sophisticated investors. Along with traditional market risks, marketable alternatives are also subject to higher fees, lower liquidity and the potential for leverage that may amplify volatility or the potential for loss of capital. Additionally, short selling involved certain risks including, but not limited to additional costs, and the potential for unlimited loss on certain short sale positions.