The stock market continued its stair-step higher in Q2 amid slow but steady economic growth, decreasing inflation pressures, and low volatility on both the interest rate-front as well as equities. GDP growth started off this year on a lackluster note, but growth picked up in Q2 and is estimated to be stronger again in Q3. And this has come without rising bond yields and without escalating inflationary pressures, leaving investors to wonder if we are back in a “Goldilocks economy” like the one that characterized much of the mid- to late-1990s?

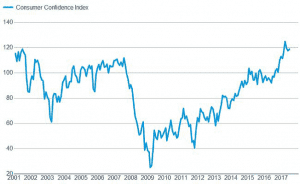

Markets can thrive in an environment of steady growth and low inflation. Both small businesses as well as consumers have responded positively to this combination, which is one of the reasons that confidence surveys (see below) remain near multi-decade highs. This should help reinforce a positive feedback loop for the economy with steady job growth supporting consumer spending and continued corporate profit growth supporting stocks.

The Federal Reserve took advantage of the steady economy and markets to squeeze in another quarter point rate hike in June. As it continues to exit the period of extraordinary monetary policy that followed the 2008-09 recession, the Fed also discussed reducing its oversized balance sheet. Recall that as a result of its asset purchasing program (“QE”), the Fed’s balance sheet grew to $4.5 trillion in recent years. The Fed stopped adding to its balance sheet in 2014, but they have been reinvesting the proceeds of maturing assets in new securities to maintain the overall value.

The Fed is now talking about allowing these securities to start to run-off its balance sheet in a measured manner. They would start by allowing $10 billion per month to roll off without reinvestment, and let those amounts rise each quarter. Ultimately they see this plan allowing for a maximum of $50 billion per month to come off its balance sheet. No exact timetable has been set for the start of this process, but recent comments have led many to expect September as a reasonable time.

Considering the Fed has hiked interest rates four times this cycle and is discussing a two-pronged approach towards “normalizing” monetary policy, it is surprising that long-term bond yields haven’t risen more. One of the reasons for this is that bond yields are sensitive to inflation pressures, which have been easing in recent months. An example of this can be seen below in the chart of the CRB Commodity Index, which remains mired in a multi-month downtrend. Yet despite the lack of inflation, the Fed still expects to raise rates one more time in 2017 and up to three more times in 2018.

Of course, the Fed’s forecast of future rate hikes does have a spotty track record. It remains to be seen how the markets will react to the balance sheet runoffs and further interest rate hikes. If volatility picks up, economic growth slows, or inflation continues to fall it could cause the Fed to pause its rate hikes earlier than planned.

Another area of the financial markets where volatility has been historically low is the stock market. A measure of market volatility known as the volatility index (VIX) recently hit the lowest levels in over 10 years. As such, recent pullbacks in the market have been brief and shallow. Investors sitting with cash and waiting for a correction have had few good buying opportunities. The last 10% correction in the stock market was in February 2016. The 2 steps forward, one step back pattern appears firmly in place for the time being.

While certain market pundits and media outlets continue to look for holes to poke in this market, the truth is that it’s hard to argue with the current goldilocks environment. The stock market likes this not-too-hot, not-too-cold backdrop where steady economic growth isn’t so strong that it stokes inflation but also isn’t so weak that companies can’t grow profits. Overall investor sentiment is far from bullish and complacent, and from a contrarian perspective that leads us to believe that there is still room for this market to run.

Jordan L. Kahn, CFA

Chief Investment Officer

Sources: Stockcharts.com; BTIG research; Raymond James; Briefing.com; IBD; Standard & Poors; Barron’s; Charles Schwab