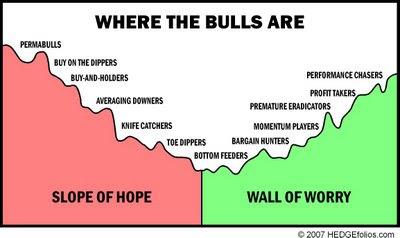

Stocks got off to a strong start in Q1 2017, despite the myriad of calls that the market was overvalued and stocks were overdue for a big correction. Despite all of the negative headlines in the media, worries over geopolitical events, delays in Washington, etc., stocks have experienced less than a 3% pullback so far this year. The situation exemplifies the old adage that ‘a bull market loves to climb a wall of worry’.

One area that market pundits have called into question is the strength of the US economy (GDP growth). Q1 growth estimates have been coming down steadily, which led some to conclude that the post-election boost to the economy was short-lived. An interesting phenomenon that has surfaced in recent years has been the seasonal pattern of weakness showing up in Q1 GDP figures. But extrapolating that weakness as a tell for the remainder of the year has proven to be a mistake. We think that pattern will hold again in 2017, and that economic growth will pickup in the back half of the year. As the chart below shows, the Philly Fed Index has been a good leading indicator for the overall economy. Thus, the recent uptick in the index bodes well for a pickup in economic growth to follow.

Another indicator that may be leading market strategists astray is the yield curve (i.e. – the term structure of interest rates). The Federal Reserve recently hiked interest rates, putting upward pressure on short-term bond yields. Around the same time, long-term bond yields began to come down. This “flattening” of the slope of the yield curve is often and indication that the bond market is forecasting slower growth ahead. But other factors can affect long-term bond yields as well.

Whenever geopolitical tensions rise (think N. Korea, Syria, French elections, etc.), buying demand for safe-haven US Treasuries increases. As prices of Treasuries rise, bond yields fall. Another factor depressing bond yields could be that many hedge funds and traders have been forecasting higher bond yields, especially after the sharp rise in yields witnessed in the aftermath of the election. As such, these traders made large short bets on Treasuries. But as Treasury prices have risen in recent weeks, these short bets have resulted in large losses, leading to short-covering which only exacerbates the trend.

For its part, the Federal Reserve has stayed on message that economic growth is firming. They have used every opportunity to reiterate to investors that they anticipate raising short-term interest rates three times this year. We know from past years that if the Fed wasn’t confident in this outlook, or if they were forecasting growth to wane in the coming months that they would take a pause from raising interest rates. But this has not been the case.

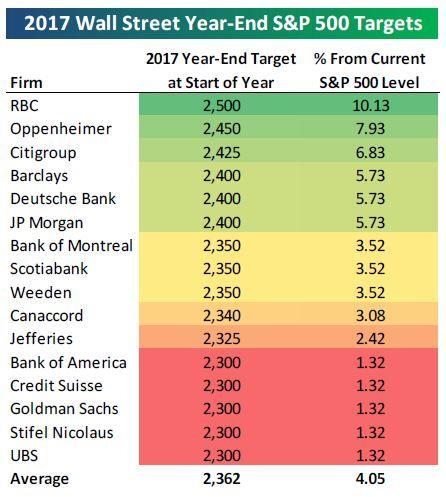

So far we have identified examples of the ‘wall of worry’ with respect to GDP growth; we have seen examples in the message from the bond market; but the strongest example is likely coming from the stock market, which continues to defy conventional wisdom that stocks have run too far-too fast. Coming into 2017, consensus forecasts from Wall Street strategists about the prospects for the stock market were tepid at best. As the chart below shows, the median forecast for the S&P 500 Index was for the market to rise roughly 4% for the year. Stocks have already surpassed those forecasts in Q1.

Even without the prospects for health care reform, tax cuts, and repatriation, corporate earnings growth bottomed late last year and was poised to rebound. That is being reflected in stocks, and is likely to continue in the intermediate-term.

One must always add the caveat that while market corrections can and do occur at any time, the next correction will not spell the end of this bull market. We are always mindful to pay attention to red flags on the horizon, but right now our advice is to stay the course.

As always, we encourage you to contact us to review your accounts and update us on any changes that may affect your personalized investment advice.

Jordan L. Kahn, CFA

Chief Investment Officer

Sources: Stockcharts.com; BTIG research; Raymond James; Briefing.com; IBD; Standard & Poors; Barron’s; Charles Schwab