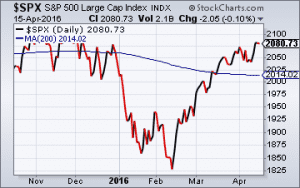

Market volatility: If you only looked at how the stock market started and finished the first quarter of 2016, you would probably wonder what all the fuss was about. After all, stocks were basically unchanged, right? But zooming in from the forest to the trees shows a much different picture. Stocks began the year in sell mode and suffered steep losses into mid-February. At that time, bearish sentiment was hitting extreme levels and investors were convinced a new bear market was upon us.

As we remind clients frequently, markets rarely move in a straight line. There are always bounces along the way. Sure enough, in mid-February stocks had already declined -11% for the year and were due for a bounce. The catalyst came from oil prices bottoming, some high profile insider buys, and short-covering in stocks. The surprising aspect of the ensuing bounce was not that stocks staged a rally, but rather the steady buying demand that propelled stocks higher for the next two months.

As of this writing, stocks have spiked 15% from their intraday lows in February. That is a nice bounce and a welcome change of sentiment for investors, but viewed through a historical context it isn’t something that would cause us to abandon our recent cautious stance. Snapback rallies are a normal part of investing, but we look for confirmation from underlying corporate earnings growth, strengthening economic indicators, as well as confirmation from the credit markets before being swayed by the price action in stocks alone.

If the backdrop to the investment landscape continues to improve in the coming months, we will factor that into our forecasts and portfolio positioning. But at this juncture we feel that the drop in market volatility back to extremely low levels could be lulling investors into a false sense of security and complacency. From OPEC decisions on oil, to the possibility of a “Brexit”, to the upcoming Presidential elections, we see plenty of catalysts on the horizon that could cause a flare up in market volatility. Additionally, we have not yet seen the additional confirmations we look for from other market-based and economic indicators.

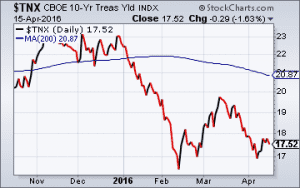

Fixed income: For all the talk about the economy strengthening and interest rates moving higher, the action in the 10-year Treasury bond year-to-date has been the opposite. To wit, the yield on the 10-year T-note began the year at 2.27%. Since then it has fallen over -20% to levels near 1.75%. That level might seem awfully low at first glance, but a look at bond yields around the globe paints a surprising picture. The chart below shows that bond yields in the U.S. are actually relatively high compared with most other developed economies.

Moreover, there are a few countries that have actually pushed rates into negative territory. Go figure. With bond yields so low across the globe, we would anticipate continued downward pressure on rates in the U.S., where yields likely still look attractive relative to bond yields in many other countries. In mid-2012, yields in the U.S. sank to 1.40%. If economic growth continues to slow we think it is reasonable to see yields test these multi-year lows again.

The Federal Reserve raised interest rates 0.25% back in December 2015, and at the time indicted its internal forecast for an additional four rate hikes in calendar 2016. But after the severe bout of market volatility earlier this year in conjunction with slowing global economic growth, the Fed ratcheted back those expectations and indicated only two rate hikes may be appropriate this year. We think even that could be a stretch. For one, the Fed rarely if ever moves ahead of a Presidential election (for fear of looking political). So we would put the odds closer to one rate hike, if at all, and not until after the election. Of course, there is a lot of time between now and then for shifts in the financial landscape.

Economic growth: Coming into this year, consensus forecasts for first quarter GDP growth in the U.S. were right around +2.5%. As more economic data was released these forecasts began to see slight downward revisions. One popular model with a good track record is the GDPNow forecast put out by the Federal Reserve of Atlanta. As seen in the graph below, while their forecasts bounced around quite a bit in the first quarter, more recently they have fallen dramatically. Their current estimate for Q1 GDP growth is now just 0.1%. That is quite a slowdown, with virtually no growth projected at the moment. Of course, things could bounce back nicely in Q2 and make Q1 look like an outlier, but big picture it fits with the thesis that global economic growth continues to slow from 2015 highs.

Talk of slowing global growth started with China, now the world’s second largest economy. For all of 2015, China’s economy grew +6.9%. While that figure looks high compared to most countries, it was actually the slowest growth rate for China in 25 years. And for first quarter of 2016 growth looks to have slowed further to 6.7%. China is desperately trying to “manage” their slowdown and their real estate bubble, both of which make for a daunting task. Regardless of their attempts to keep the economy growing, the protracted slowdown will continue to have an effect on overall global growth.

Summary: Our big picture thesis remains that as global economic growth slows, as well as growth in the U.S., it puts downward pressure on corporate earnings and thus the stock market. Consensus earnings estimates for the S&P 500 companies in 2016 have already been revised downward by -7% since January 1st. That puts the P/E multiple of the market near 17.5x, a lofty valuation. Additionally, the drift lower in bond yields is an implicit forecast of slower anticipated growth. For us to become incrementally more bullish, we would need to see changes in all three: 1) downward revisions to earnings halt and turn higher; 2) forecasts for GDP turn up; and 3) an increase in bond yields that signaled greater optimism for growth.

Jordan L. Kahn, CFA

Chief Investment Officer

Sources: Stockcharts.com; BTIG research; Raymond James; Briefing.com; IBD; FT.com; Barron’s